Learn the Myths and Facts About Qualifying for a VA Loan

VA loans are a great benefit for any veteran.

Not only do they generally come with a lower interest rate than you could find with a traditional loan or even an FHA loan, they also don't require any money down.

That means you can get into your new home sooner and start building equity, taking advantage of tax benefits, and even saving money every month if you live somewhere where it's cheaper to buy than it is to rent.

But when it comes to understanding the benefit, a lot of veterans don't know it's available to them. Or worse, they believe some of the myths out there about the loans and decide not to use the benefit at all.

Make sure you know what's fact and what's fiction so you don't end up losing out on some seriously great benefits.

Don't be fooled by myths about VA loans

VA loan lenders hear the myths all the time. They can keep you from taking advantage of a benefit that would help you become a homeowner and save a lot of money while you're doing it.

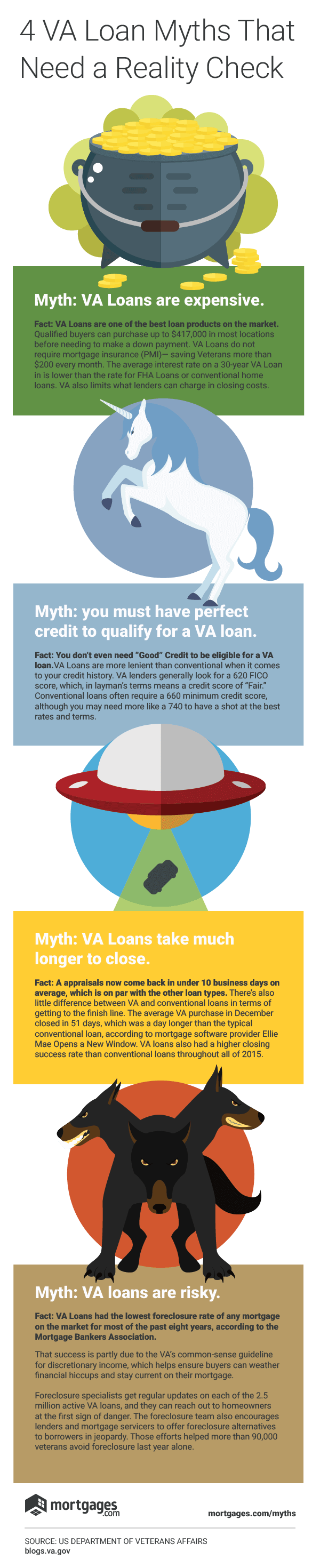

Myth #1: You need excellent credit

There's technically no credit limit for a VA mortgage. Why?

Since the loans are backed by the federal government, there's a much lower risk for lenders. That being said, you should still work on improving your credit if you're going to apply because it will help you get even better rates and terms.

Myth #2: They're a scam

It's true there are a lot of people out there running VA loan scams and general mortgage scams. But if you're going through a qualified lender, these loans are actually one of the best options available to a veteran.

Myth #3: They take a long time to close

VA mortgages don't take any longer to close than traditional mortgages. In fact, in a lot of cases they're more likely to close and close faster.

Myth #3: They're risky

VA loans are actually more stable than traditional mortgages.

Why? They come with an income requirement, which helps ensure the borrower can afford their loan and they're tracked by the Loan Guaranty Service. If a home buyer is more than 60 days late on their payments, the Loan Guaranty Service will work with you and your lender to find an alternative to foreclosure.

Myth #4: You can only use them once

One of the really nice things about a VA mortgage is you apply for it as many times as you need to. That's great news for active military who might end up moving multiple times before they retire.

Myth #5: They're expensive

You can use your VA loan benefits for a loan up to $417,000 in most places in the US without a down payment.

Not only that, VA loans don't require private mortgage insurance (PMI), which can save you close to $200 a month. Add that to what you'll be saving thanks to your lower interest rate and the limits on your closing costs and you're looking at a pretty good deal.

So, what should you know about qualifying for a VA loan?

New myths about VA loans pop up every day and if you don't know the facts, it's hard to know what to believe. Here's what you can count on when it comes to VA loans.

They're not issued by the VA

The loans are backed by the federal government, which is one of the reasons they have such great rates and terms.

But you don't go to the VA to get them. Instead, you'll get your Certificate of Eligibility through the VA and your loan through a qualified lender.

You have to live in the home you're financing... but it can still be an investment property

VA loans are designed specifically for your primary place of residence. But you could use your VA home mortgage loan to buy a multi-family building with up to four family units and one business—if you're willing to live in one of them.

You can use them more than once

Your funding fee will be a little higher the second time you use the loan program, but you can use it multiple times if you want to.

You'll have to pay a fee

Each VA loan borrower is required to pay a funding fee. The amount is based on your military category, your disability status, and how many times you've used the benefit before. The fee helps reduce the burden to the taxpayers if you end up defaulting on the loan.

You can use them to refinance a home or make improvements

VA loans aren't just for new purchases. You can also use them for cash-out refinancing.

The only thing that will change is your funding fee. You may be able to use a VA home mortgage loan to make improvements on your existing house that make it more energy efficient or to add accessibility features to the home.

They're easier to get than a traditional loan

Since the loan is insured by the federal government, lenders can approve you with lower credit scores and no money down—something that would be virtually impossible with a traditional loan.

You can pay them off early—with no pre-penalty fee

Lots of traditional loans will charge you a fee if you pay your home loan off a certain amount of months before you're scheduled to. That fee helps ensure lenders they'll be able to make money through interest.

If you get a VA mortgage, you'll be exempt from that fee.

Interested to see how much your VA loan could cost you from month to month?

Utilize our special VA Loan Calculator to figure those numbers out. We'll estimate your taxes, your insurance payment, your VA funding fee, and more. Use this handy tool today!

You can get them while you're deployed

As long as you have someone to handle things stateside and you can prove you're alive and well, you can use your benefit while you're deployed. Find out how.

They're not just for veterans

True, these benefits are designed for veterans, but there's also a provision to allow the surviving spouse of a deceased veteran to claim the benefit.

According to the VA's website, one of these conditions must be met for spouses:

-

Unremarried spouse of a veteran who died while in service or from a service-connected disability, or

-

Spouse of a servicemember missing in action or a prisoner of war

-

Surviving spouse who remarries on or after attaining age 57, and on or after December 16, 2003

(Note: a surviving spouse who remarried before December 16, 2003, and on or after attaining age 57, must have applied no later than December 15, 2004, to establish home loan eligibility. VA must deny applications from surviving spouses who remarried before December 6, 2003, that are received after December 15, 2004.) -

Surviving spouses of certain totally disabled veterans whose disability may not have been the cause of death

You can pair them with a state program

Lots of states have local benefits for veterans who buy a home in their state. Depending on where you live you might be eligible for reduced property taxes or other benefits—check your state's VA website to find out.

You get it. VA loans are great. So, how do you get one?

Your lender will be able to give you specifics when it comes to the exact numbers you need. If you meet those qualifications all you have to do is prove you're eligible for the loan. For most qualifying veterans, proving your eligibility is relatively easy. You'll just need the following.

A DD-214 or Statement of Service

There are two options for the first form. Which one you use depends on if you're on active duty, in the reserve, or have been released or discharged.

If you're no longer on active duty, you'll need your DD-214, otherwise known as your Certificate of Release or Discharge from Active Duty. If you can't find that form, you or your VA-approved lender can request a new one from the National Personnel Records Center.

If you're in the reserve or on active duty, you'll need a Statement of Service on official letterhead, signed by the adjutant, personnel officer or commander of your unit or higher headquarters. It should include all of your basic information:

- Full name and date of birth

- Social Security number

- Rank, branch of service, and any previous discharge dates and types

- Date you entered active duty

- Name, title, and signature of the officer providing the statement

Certificate of Eligibility

Your Certificate of Eligibility proves to your lender that you're eligible for the VA loan benefit. All you need to do is prove that you:

- Have served 90 consecutive days of active service during wartime, or

- Have served 181 days of active service during peacetime, or

- Have more than six years of service in the National Guard or Reserves, or

- Are the spouse of a service member who has died in the line of duty or as a result of a service-related disability

You can apply for the COE yourself or your lender can apply on your behalf. Having your VA-approved lender apply is quicker.

You can also fill out a Form 26-1880, electronically or by hand, submit it, and wait for your COE to arrive. You can also ask your VA-approved lender to apply for you, which is generally a little easier, especially since you're already dealing with a lot of paperwork to buy your home.

Either way, once you've received your COE, you won't need to get another one, even if you end up borrowing from a different lender.

Once you have the right forms, you'll be well on your way to a home of your own. The VA Loan is a great benefit, and you've earned it.

Pass it on

Don't let your friends miss out on their VA loan benefits. Pass these busted myths along so they can take advantage of their VA loan benefits.

Still have questions? Get the facts about VA loans. Interested to learn how much house you can afford with a VA loan? Find out here.